Start with Your Success Scan

Both your personal credit scores and your business scores impact your initial funding.

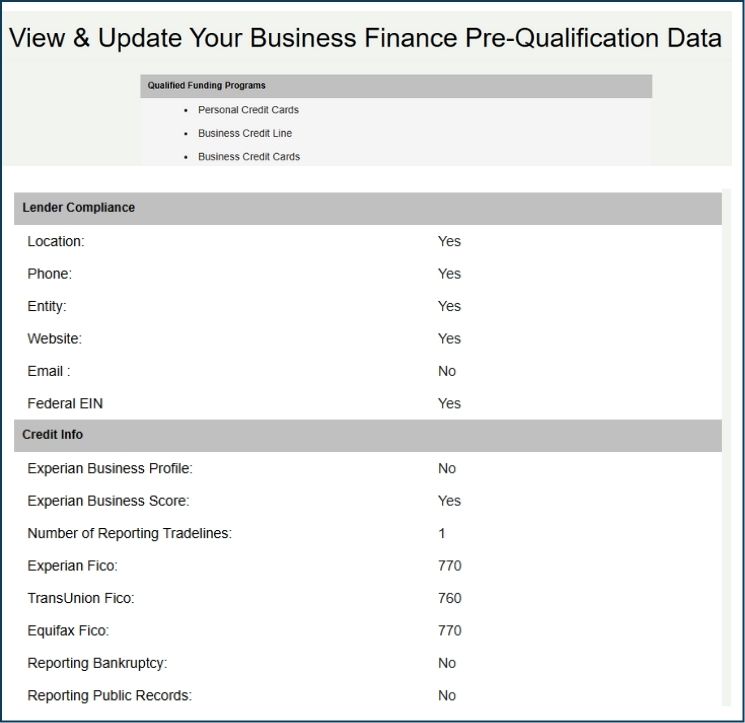

The Success Scan Tells You Your Current Funding Status

Based upon your inputs we can give you an idea of the funding programs you currently qualify for.

We also provide the status of the Lender Compliance items that you will need to have in place in order to apply. Don’t be immediately rejected because you don’t have a business address!

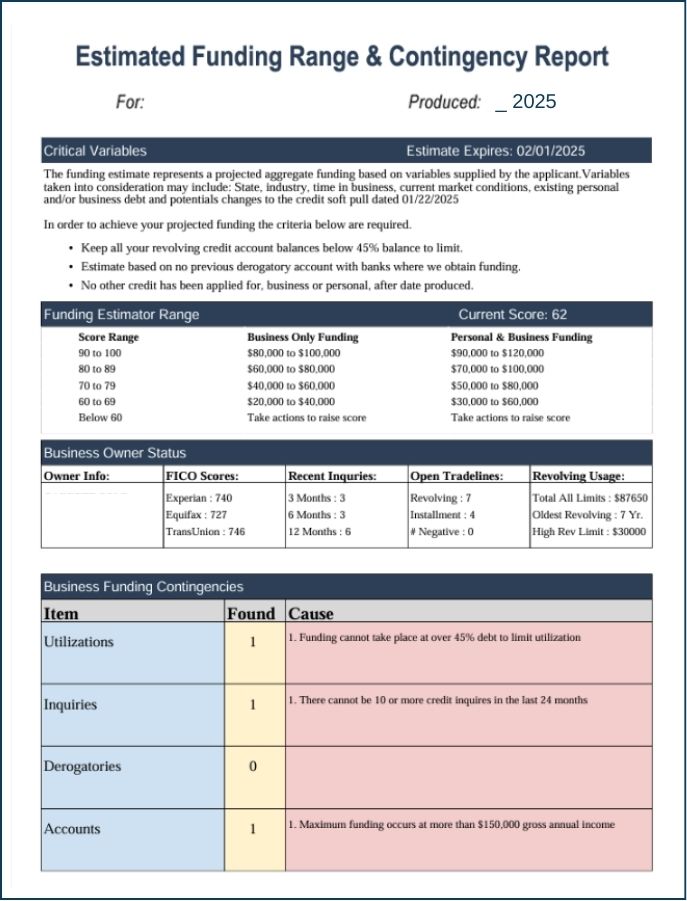

Then Request Your Estimated Funding Range

Estimated Funding Range.

Based upon your responses, we can provide you with an estimate of your initial funding amount. The higher the score the higher the amount of initial funding. Complete the Success Scan and we can review.

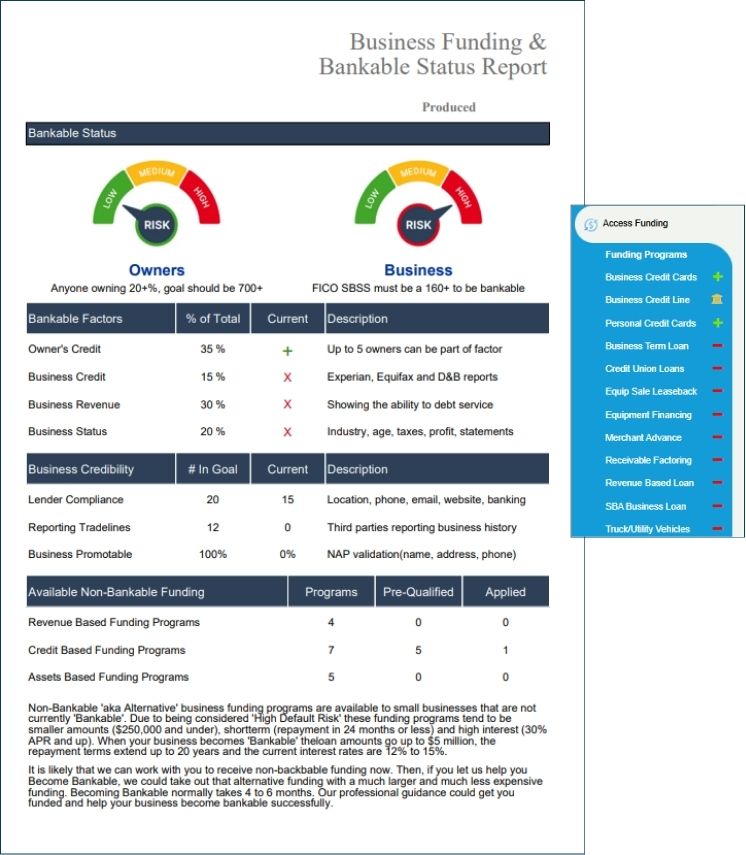

Then Enroll and See Your Status

Your Status Report

Once enrolled you will see your Status Report which helps you track your process in becoming bankable. The key is to reduce your risk in the eyes of lenders. Let’s make it easy for lenders to say yes!

Begin Monitoring Your Scores

Monitor Your Business Scores

Then each month, monitor your scores to track improvement. Your improved business scores along with solid business revenue will allow you to become bankable! You will need to subscribe to Experian and Dunn and Bradstreet.

Then Start Acting Strategically

Have Questions?

Becoming Bankable Is A Table With Four Legs

When your business becomes bankable that means you have separated personal credit from business credit and established a business entity that can stand on its’ own for financing.

Leg One – Lender Compliance – The Algorithm Gatekeeper

Lender compliance is a series of small items that a lender’s underwriting computer is going to immediately check when you apply for a business loan. Lenders are simply looking to see if your business falls into known higher rates of default. Until Lender Compliance is completed, your business will be considered high risk. Most lenders sell their loan portfolios to secondary market investors. Those investors prefer to buy low risk loan packages.

Leg Two – Business Credit History – AKA Comparable Credit

If you look at your business credit reports and you do not see at least 10 reporting tradelines, then you have too little business credit history to be considered bankable. Also if you only have $300 to $500 reporting tradelines then you do not have “Comparable Credit”. Lenders want to see that you have tradeline credit history of a comparable size to what you are asking them to approve.

Leg Three – Business Credit Scores – Maintain 70+

You are well aware of how important it is to have 700 or higher personal credit scores. For your business to become bankable it must have business credit scores of 70 or above which are just like having 700 scores personally. Unlike personal credit, there is no 30 day grace period with business credit. Business credit tradelines report “to the day”. This means if you pay even 10 days late you will be reported as “late”. Another major factor is your FICO business score which for any cash type lending from a bank or an SBA loan must be a 160 or above.

Leg Four – Business Bank Rating – Maintain Low 5+

Lenders want to see that your business has the ability to debt service or cover the monthly payment for the loan amount you are requesting. For this they are going to look at your business bank rating that will tell them if you have the money to make their payment or if it is more likely that you will default. Banking rating is based on your average daily balance in your business general ledger bank account for the prior 90 days. Having at least a “Low 5” Bank Rating is critical to becoming bankable.

Loan underwriting approvals are done by computer algorithms. Via APIs they can instantly check if your business is bankable or not. Less than ten percent (10%) of small businesses have taken the time to become bankable before applying for financing. By completing the free Business Success Scan you will see where your business stands right now in becoming bankable and you will know exactly what to do to become bankable in the very near future.

The free scan looks at 150 data points on your business and lets you know where you stand for business financing, business credit, lender compliance, and everything about your current online footprint; SEO, star ratings, local listings and more. Then, it provides a step-by-step guide how to optimize each aspect of your business funding pre-qualification, business credit scores, the owner’s personal credit scores and your online marketing success.

Lender compliance is a series of approval guidelines which lenders have selected as part of their decision making process. Typically these are items that can be easily verified in an automated environment. What this means is that when you submit a business loan application the lender’s computer system will check these lender compliance items to see if your business will make it to the next level in the loan approval process.

Lender compliance items generally do not get you approved, but they can get you declined if your entity has not completed them before you apply.

Here are a few examples of lender compliance items:

Having a business address – Lenders will check the address on your application against the US postal service database to verify if it is a residential address or a business address. About 80% of business lenders will decline “home based” businesses, so if your application tests as having a residential address you have a high probability of being declined.

Operating a business from a cell or residential phone – The phone number you list on the loan application will be checked using the Federal Communications Commission database to verify it is a business phone line, a cell number, or residentially registered phone number. In many cases, lenders will decline a business loan application where the business does not have a business listed phone number.

Having an entity – In this case, you are applying for a business loan and not a personal loan, but if your business is not its own entity (such as a Corporation or LLC), then there is no business to lend to. Without an entity, everything is on you personally, because of this it is considered a personal loan and not a business loan. Many business lenders do not make personal loans, so you will be declined.

Business EIN – A Federal “Employer Identification Number” (EIN) is kind of like your social security number, but it is for your business. Lenders will check to make sure it is in place and to make sure that it matches your business legal name exactly.

Secretary of State “Entity In Good Standing” – Many business owners file their first year documents with their Secretary of State and then forget or fail to update them annually. If that happens, it has little if any noticeable effect. Your business bank accounts still work, your EIN is still active, your phone works, etc. However, when you submit a business loan application the lender’s computers will check using your Secretary of State’s computers to see if your entity is in good standing. If not you will most likely be declined.

There are about 20 lender compliance items that your business needs to complete. They are all easy to complete and most have a free or low cost solution.

Most lenders do not check all 20 items, but you don’t know which ones they will check.

That means to be safe it is best to complete them all. Lenders never tell you which compliance items got your application declined. The agent you are dealing with does not know anything about compliance items. The compliance item check list was programmed into their system and was never disclosed to them. So it is up to you to get those items completed before you apply.

By running a business success scan you will see all lender compliance items and how to complete them.

What are reporting business credit tradelines?

Tradelines are an industry term used to describe accounts that appear on your credit reports. Therefore any account that appears on your personal or business credit reports is considered tradeline.

From a business credit perspective you should strive to have at least 10 reporting tradelines on your business credit reports. Of the 10 reporting tradelines you acquire 5 of those should be vendors offering products or services your business needs on Net Payment terms. The reason for this is to build a business credit history where lenders, vendors, and credit providers can determine how your business pays its bills. Just like on your personal credit reports if you only had one or two reporting tradelines there would not be enough credit history to accurately determine how great of a credit risk you might be. But with at least 10 reporting tradelines assessing your credit risk becomes a much easier and more accurate job.

To develop at least 10 business credit reporting tradelines you are going to need access to lenders who reports, credit providers who report, and vendors who report. Completing the Business Success Assessment will show you how many business credit reporting tradelines you have right now.

Getting 10 business credit reporting tradelines is the easy part. Knowing where to find them is the hard part and that’s one of the many services we provide.

Your business must have strong business credit scores that are separate from you personally.

It is a fact that, in today’s economy, your business needs all the help it can get to obtain the financing you need to grow and succeed. Business credit scores now play a major role in business financing and have become the determining factor in how much your business gets approved for, what interest rate you pay, and what length of payment term you receive. Most large corporate and SBA lenders have factored business credit scores into their underwriting guidelines.

Now that we have determined the need for business credit scores, let’s take a look at who reports those scores;

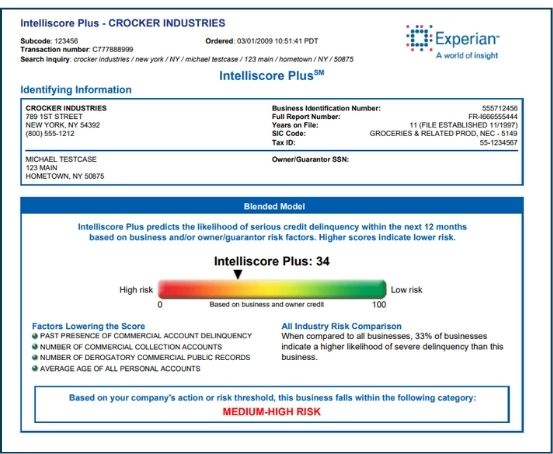

Experian Business Information Services – Experian is the leader in personal credit reporting and has ventured into business credit reporting. A trade line is any company that sends payment histories into a business credit reporting agency. If you have a business credit card, equipment or vehicle lease, or a corporate account with any large supplier or retailer they are most likely reporting to Experian Business.

Equifax Business – Equifax has been in business credit reporting for a long time. They used to be called the “Small Business Financial Exchange” and only gathered credit information from member banks. While they have branched out from this practice, their major reporters are still banks. Therefore, anything your bank knows about you so does Equifax.

Dun & Bradstreet – Dun & Bradstreet is the oldest player of the business credit reporting agencies. Dun & Bradstreet reporters are primarily vendor credit lines. These are businesses that extend credit to other businesses on “Net 30” credit terms. That means if you have vendor credit lines for products or services that give you 30 days to pay, then they most likely report your payment history to Dun & Bradstreet.

FICO SBSS (Small Business Scoring System – Just like personal FICO scores have become the standard for all things consumer lending, FICO SBSS scores have become the standard for all things business cash lending. Banks, credit Unions, the SBA, large fintech lenders, leasing companies are now using FICO SBSS in their approval process. The FICO SBSS score is not used as the standalone approval gauge as are FICO scores for personal lending but rather it is used as a method of declining applications along with factoring into the offer of amount, rate and term.

After you take the business success assessment, we walk you through first checking your business credit scores and then building strong business credit scores that can help your business obtain larger amounts of financing and on better terms.

The focus is on 10 primary small business loan programs.

These products service about 90% of the business financing needs of small business owners nationwide and these programs have the highest percentage of closing.

Here are the top ten small business finance programs:

Finance Program # 1 – Unsecured Financing. These are a spectrum of corporate credit cards available from many providers. You could apply for some of these on your own, but you don’t know their underwriting and approval guidelines. Therefore, your potential for getting declined is very high. Once you are declined 3 times for any business lending product, then you will be declined for all business lending products for at least the next six months. That is because other lenders don’t know what happened on those applications and they will wait to watch your credit reports to find out. Typical approvals for business credit cards are $25,000 to $150,000.

Finance Program #2 – Revenue Based Loan. Your gross revenue is the primary concern. If your business has consistent gross monthly revenue, then this loan program may be for you. It is easier to get approved for than business credit cards. Repayment is done Monday through Friday via automated clearinghouse from your business checking account. Typical approvals for business revenue based loans are $10,000 to $250,000. This program normally funds 10% of your annual gross revenue.

Finance Program #3 – Business Term Loans. If your business has tax returns for the last two years showing at least $250,000 in gross annual revenue, then you maybe be a good candidate for this program. The program funds between $50,000 and $500,000 to existing business who plan to use the funds for growth.

Finance Program #4 – Equipment Financing. Many times we find that business owners are seeking financing to buy “things”. Some of these things may include computers, office furniture, software, vehicles, forklifts, machinery, or other hard goods; and most can be financed on their own without having to use valuable cash flow to do so. Equipment financing is available from $10,000 to $5,000,000 and can be bundled with other funding programs.

Finance Program #5 – Investment Rollover. Most small business owners don’t realize that there is a provision in the tax code that allows them to roll their retirement investment accounts into an investment in their own business and avoid the tax penalties for taking the money out. If you have at least $35,000 in retirement investment accounts, then this business financing product may be for you.

Finance Program #6 – Account Receivable Factoring. If your business has open invoices from other businesses that owe you money, those invoices can be turned into cash. This program has many benefits. First, it can give you access to fast cash. Next, you no longer have the burden of trying to get paid. Lastly, you can now offer Net 30 day credit payment terms to your business clients. Account Receivable Factoring is available from $10,000 to $30,000,000 and can be bundled with other funding programs.

Finance Program #7 – Purchase Order Financing. If you find that you have an open purchase order for finished goods that you have trouble filling, then Purchase Order Financing may be right for you. Purchase Order financing is available from $10,000 to $30,000,000 and can be bundled with other funding programs.

Finance Program #8 – Credit Union Loans. Credit Unions have started to come back into business lending in a big way. The rates are usually lower than other types of loans, terms may be better, and they tend to be easier to qualify for.

Finance Program #9 – SBA Express Loans. The SBA Express program provides for quick reviews and smaller loan amounts. The SBA responds within 36 hours and the loan range is $25k to $350k. Funds can be advanced in the form of working capital, a line of credit, or commercial real estate loan. The program can be very fast for $50,000 and less.

Finance Program #10 – Vendor Trade Financing. 95% of all business lending is done Business-to-Business and not lender to business. Once you complete the Business Success Assessment you gain access to a searchable database of over 3,000 vendors that offer Net 30, 60, 90 day payments terms.

Once you complete the Business Success Assessment you will know which of these funding programs your business pre-qualifies for now and exactly how to pre-qualify for them in the future.